The newest announcements on the Shipping Emissions front has been the declaration of a ‘Net Zero GHG emissions target’ by the year 2050. A case wherein the International Maritime Organization (IMO) had to backtrack from its initial goal of 50% post the industry itself being aggressive on its targets. While Breakbulk and MPVs forms a significantly smaller portion of cargo and vessels, unlike its container counterparts where the top players have set net-zero emission targets around 2050- ranging from as early as 2040 to as late as 2060 (something that may now warrant a revision), the Multi-purpose vessel players are yet to provide aggressive targets in terms of emissions.

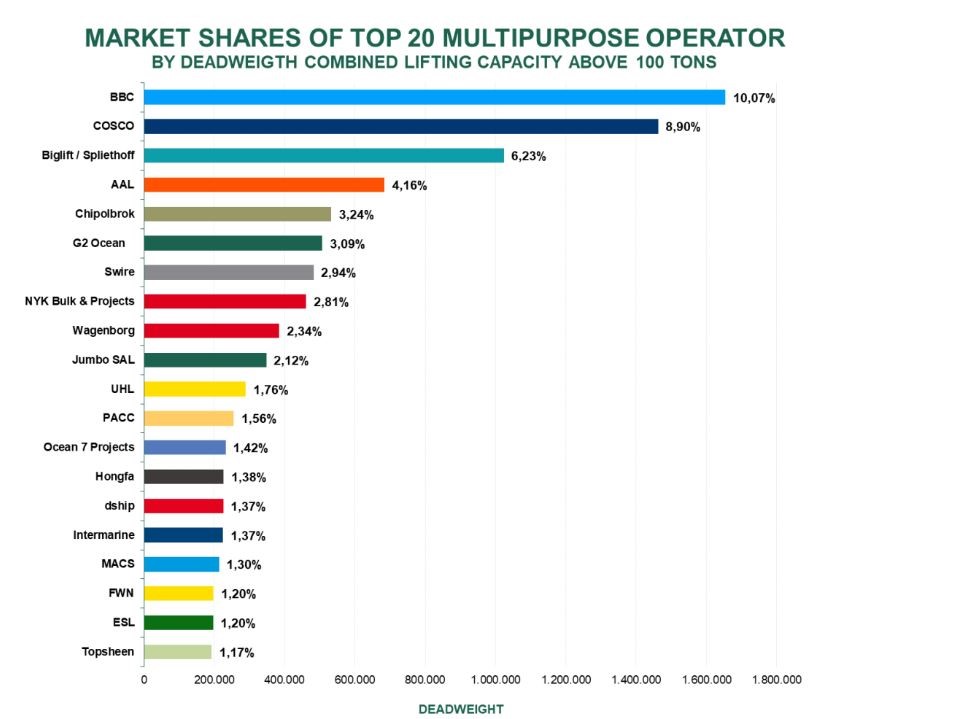

While Breakbulk and MPVs forms a significantly smaller portion of cargo and vessels, the fact that there are hardly about 25 newbuilds in the sector and the added effect of aging fleet could be something that the Project cargo industry may be wary about and in the lookout for. A sneak peek into their market share alone signifies the nature of the sector and gives us a picture of how fragmented the market has been. An interesting comparison reveals that the total deadweight of vessels in the MPV sector with a combined lifting capacity of over 100 Tons is about 16 Million Deadweight, and the total new-builds under progress is merely 3% as against nearly 30% for the container fleet sector. This is despite the fact that Breakbulk prices have dipped a mere 61% from its peak level witnessed in July 2022, as against a near 87% dip in container prices. The Multi-purpose prices are still over 2.25x over their pre-pandemic levels while container prices on most key trade lanes are just a fraction above the pre-pandemic levels or in some cases, dunked significantly below.

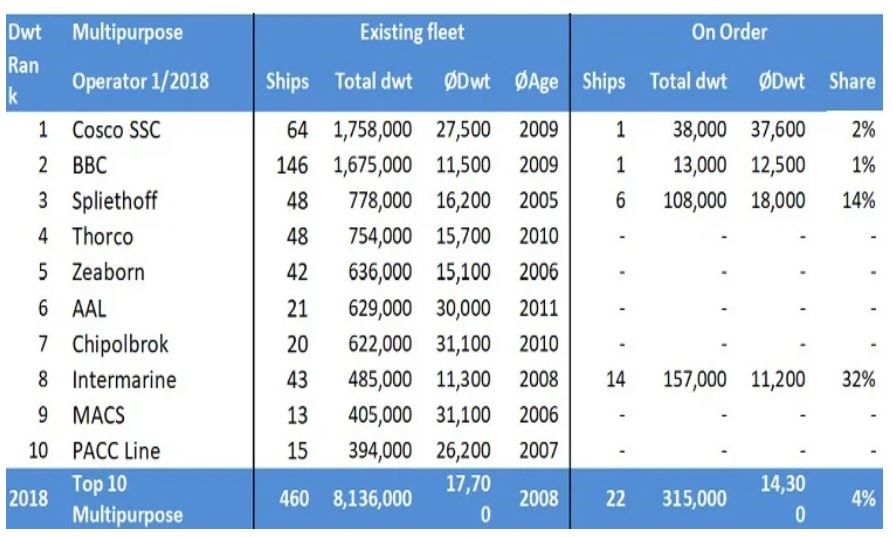

While the top 10 operators share about 45.9% of the market share, none outside the top 10 have a market share of even 2%. Some data from 2018 reveals that the average age of the fleet had been around 10 years for all the major operators. With not much newer vessels on the horizon and a major chunk of the incumbent fleet in the market booked for offshore purposes, and assuming that a significant portion of the fleet weren’t added we are ideally looking at a global MPV fleet where the average age is 15 years. Another half a decade, and they would be drawing up plans for recycling/ scrapping. While the overall demand of the sector isn’t high with other sectors jostling for a pie of the Breakbulk cargo, there is still demand for deck carriers and project cargo, and the sector has to ramp up its newbuilding plans to oversee and account for the demand that can come in the long term, but also account for smarter, efficient and greener vessels in line with the industry’s footing on emissions, which are much welcome.

Image sources: Toepfer (Market Shares of Top 20 Multipurpose Operators- 2023) and Maritime Executive (Market Shares of Top 20 Multipurpose Operators- 2018)

Acknowledgments go to our guest writer, Mr. Gautham Krishnan, for his valuable contribution to the article.

Author of the article- Gautham Krishnan: Gautham Krishnan is a logistics professional with Fluor Corporation, in the area of project logistics and analytics, and has worked in the areas of Project Management, Business Development and Government Consulting.