Estimated reading time: 2 minutes

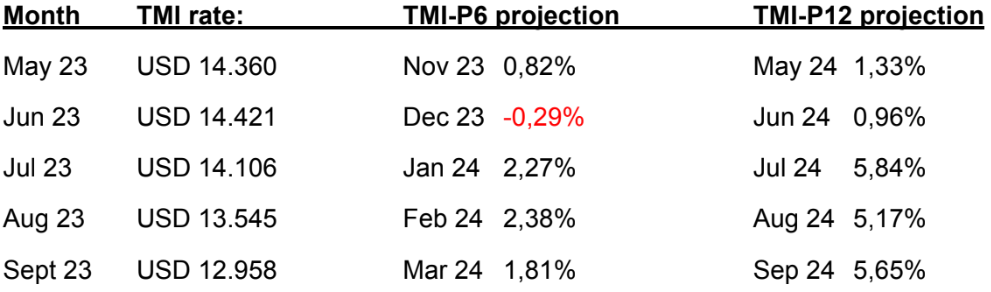

The set of latest expected figures over the next 12 months for the Multi-purpose Index (MPP) are expected to rise, based on the outlook from different stakeholders. The projected data from Toepfer’s analysts speak of greener shoots starting from January 2024, post a subdued Q4, 2023. The expectation has been of the expected future demand owing to the number of projects. However, the reality has yet to condition or trigger the first shoot of green, as the Toepfer’s Multipurpose Index, over its latest quote dived below the psychological mark of USD 13,000- and in the process, hovering just about 5-6% over the post-pandemic averages. There is a split verdict on the freight street on if this is the bottom for now.

We witnessed the volatile swings in container trade wherein indices rose up by about 20% between July and September, only to fall to the same extent or even more, despite a horde of issues ranging from the port strikes in Canada to the drought effect in Panama. That’s a clear case of abysmally low demand, in spite of all the economic headwinds projected and practiced. Now, while the project cargo sector is totally different, in terms of gauging demand – with a clear case of rising energy, defence, infrastructure needs – the demand thus far has been stable. The rates on the shortsea side haven’t been great either.

In fact, the Toepfer’s Shortsea Index- TSI 35 has been buckling lower to end at USD 3,672- a figure last seen 30 months ago. Its counterpart the TSI-52 too had edged lower to USD 4,945- a near-two year low. How would the effect of price swings be beneficial for shippers, and would this induct a relook towards contracting flexibility, remains to be seen.

Author of the article: Gautham Krishnan

Gautham Krishnan is a logistics professional with Fluor Corporation, in the area of project logistics and analytics, and has worked in the areas of Project Management, Business Development and Government Consulting

Reference: Toepher / PCJ