Companies face heightened scrutiny in collecting, reporting, and organizing emission-related metrics. This surge in responsibility extends its tendrils into various facets of business operations, from corporate partnerships and supply chain logistics to compliance requirements and data integrity.

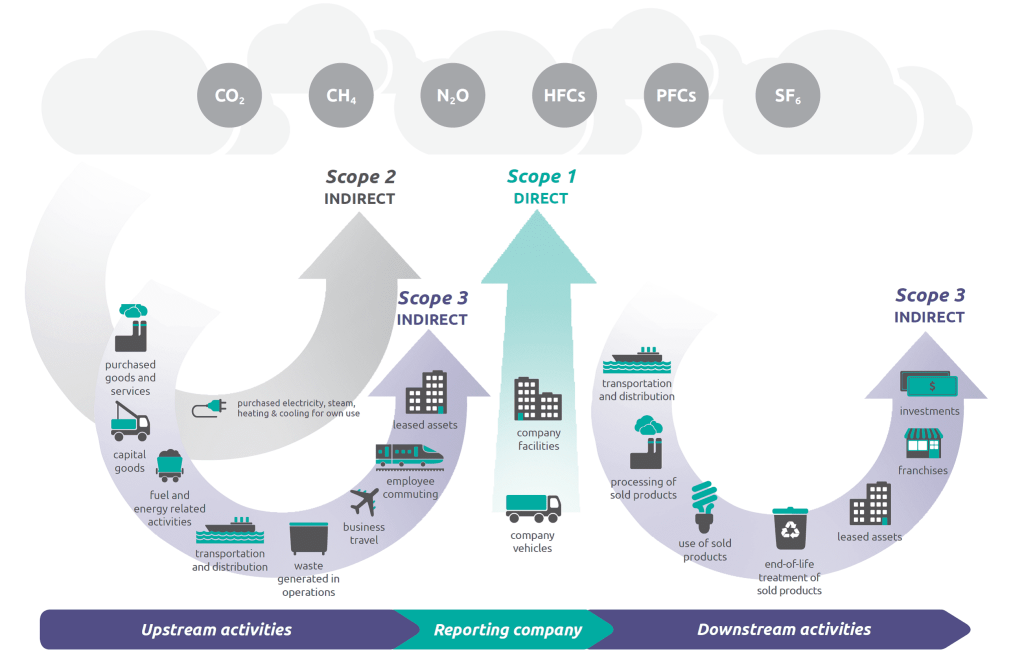

Most reporting statutes mandate or will soon mandate companies to furnish data encompassing their Scope 1 through 3 emissions. The recent emphasis on Scope 3 emissions poses a challenge, demanding an end-to-end value chain reporting approach. This compels companies to scrutinize emissions upstream, internally, and downstream to fulfill regulatory needs and the escalating demand for verifiable data from downstream customers. Mastery of the scopes is pivotal in structuring data. The Corporate Sustainability Directive adds another layer, necessitating reporting on materiality conceptual guidelines, double materiality, impact materiality, and financial materiality.

European Union’s Stricter Mandates

With the advent of the Carbon Border Adjustment Mechanism (CBAM) and the Corporate Sustainability Reporting Directive (CSRD), any major enterprise eyeing business in the European Union faces a robust obligation. This involves reporting data encompassing environmental risk, procurement statistics, and supply chain impacts. For instance, the permanent CBAM system, effective from January 1, 2026, demands importers annually declare the number of goods imported into the EU in the previous year along with their embedded greenhouse gas (GHG) emissions.

Global Impact of Stricter Reporting

Internationally, requirements for stringent reporting on intricate metrics are on the rise. The additional pressure for sustainability data reverberates through business operations, employee responsibilities, candidate recruitment, and company performance metrics. Priorities are shifting, involving additional personnel who might have been overlooked previously.

As regulations gain strength, an increased focus on data architecture becomes pivotal for seamless and continuous reporting. To offer a holistic view of sustainability reporting, data from diverse systems must be consolidated into a unified environment. Staying aware of regulations is crucial to preparation and equipping your company with the tools needed to stay compliant.

Adopting Reporting Frameworks

In 2021, a staggering 99 percent of S&P 500 companies reported ESG-related information. While lacking a single standardized reporting framework, voluntary frameworks such as Sustainability Accounting Standards Board (SASB), Global Reporting Initiative (GRI), International Sustainability Standards Board (ISSB), and Integrated Reporting Framework provide structures for organizing data. These frameworks offer insights into future expectations set by regulatory bodies.

Building Sustainable Data Architecture

Creating a data architecture designed for annual use is paramount. A database that is legible, accessible, and accurate ensures a solid baseline for future reporting. Automating data collection, where applicable, reduces human intervention, minimizing errors that could compromise data integrity.

Widening the Scope: Holistic Data Collection

Sustainability reporting draws from various organizational sectors, including manufacturing operations, EHS, HR, supply chain, and procurement. Identifying and rectifying inefficiencies in sourcing environmental data during financial reporting can save time, effort, and resources.

In a world where regulatory pressures escalate, companies must not only meet reporting requirements but also build robust systems that enhance data integrity, ensuring a sustainable and responsible business landscape.

Source: logisticsviewpoints