April 2024 has brought significant shifts in dry bulk financial landscapes. Let’s delve into the key developments shaping the industry this month.

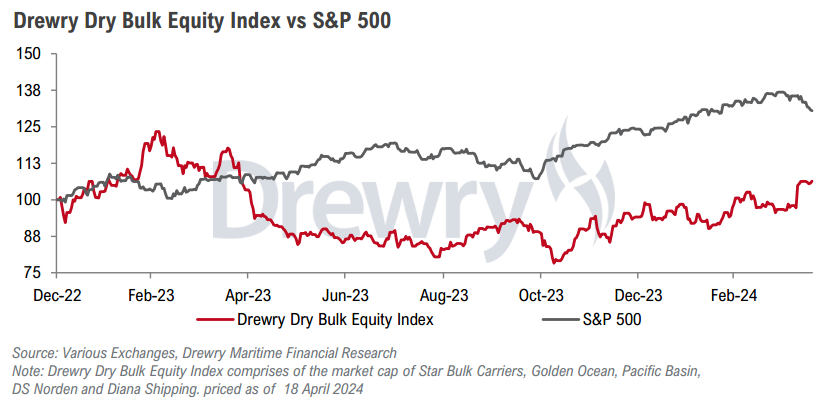

In March, the Drewry Dry Bulk Equity Index experienced a dip of 3.9%, contrasting the 2.3% rise of the S&P 500. However, April saw a remarkable reversal, with the index surging by 10.4% (as of April 18). This upswing was predominantly fueled by the finalization of the merger between Star Bulk and Eagle Bulk, propelling Star Bulk’s market capitalization and consequently boosting the overall index.

Despite a robust demand for coal at the onset of summer, charter rates faced a setback at the beginning of April. This decline was triggered by reduced tonne-mile demand following the collapse of the Baltimore Bridge and the subsequent closure of the Port of Baltimore.

However, the past week witnessed a resurgence in charter rates, ignited by heightened tensions in the Middle East surrounding the Israeli-Iranian conflict. While the conflict itself may not directly affect dry bulk trade volumes, the potential closure of the Strait of Hormuz could induce a surge in oil prices, indirectly impacting the demand for goods transported globally.

In terms of stock performance, April presented a mixed bag. While Pacific Basin saw a remarkable 7.0% surge driven by a revitalized Chinese economy and the announcement of a USD 40 million share buyback, Golden Ocean experienced a modest rise of 0.6%. Conversely, Star Bulk and DS Norden witnessed slides of 1.6% and 0.2% respectively, with Diana Shipping remaining relatively stable.

The eagerly anticipated merger between Star Bulk and Eagle Bulk was greenlit in April, catapulting the combined entity to the second position globally in terms of vessels and capacity, just behind COSCO Shipping Bulk.

Additionally, preliminary indications of 1Q24 results have surfaced, with Pacific Basin disclosing a trading update. Despite a challenging market period, the company reported an average TCE rate decline of 18% YoY for Handysize vessels, with no change for Supramax. Looking ahead, Pacific Basin has secured promising coverage for 2Q24.

Finally, asset prices have been on an upward trajectory, propelled by limited availability in shipyards and a low orderbook-to-fleet ratio. Notably, the prices of five-year-old Capesize and Panamax vessels witnessed substantial increases of 20.0% and 8.8% respectively in 2024.

Source: drewry