In the dynamic realm of global maritime commerce, the MABUX bunker indices navigated through Week 32 with subtle yet significant fluctuations, revealing a landscape of moderate growth. The indicators that steer the course of the shipping industry exhibited intriguing shifts, offering insights into the prevailing conditions and potential market trajectories.

The 380 HSFO index, a compass for heavy-sulfur fuel oil, displayed a discernible uptick, ascending by $3.83 USD from the previous week’s $554.65 USD/MT to anchor at $558.48 USD/MT. Its counterpart, the VLSFO index, representing the voyage of low-sulfur fuel oil, embarked on a similar voyage of ascension, adding $5.44 USD to its value, marking a notable ascent from $657.20 USD/MT to $662.64 USD/MT. The MGO index, a reference point for marine gas oil, followed suit, surging by $2.86 USD from $926.57 USD/MT to $929.43 USD/MT. However, as the ink met paper, no definitive trend etched its presence on the maritime map.

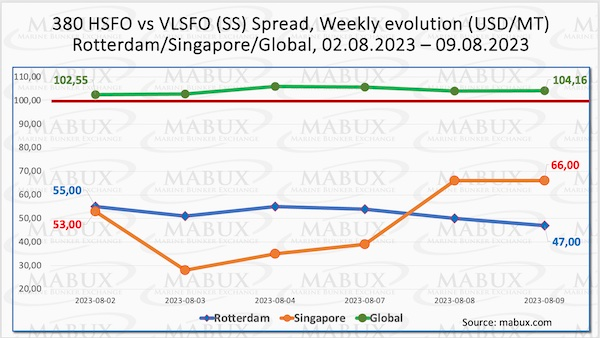

The intriguing dance of figures was mirrored in the Global Scrubber Spread (SS), which illuminates the gap between 380 HSFO and VLSFO prices. The pendulum of the SS inched up by $1.61, reaching $104.16 USD, contrasting the previous week’s $102.55 USD. Yet, beneath this incremental shift lies a tale of fluctuations. Rotterdam’s SS Spread embarked on a downward spiral, descending from $55.00 to $47.00, breaching the $50 mark and painting a picture of market metamorphosis. In Singapore, a different tide swelled, as the price chasm between 380 HSFO and VLSFO expanded by $13.00 to $66.00 USD, echoing the narrative of change. Amidst these numerical narratives, the global ports’ SS Spread journeyed beneath the $100 mark, steering toward a landscape favoring low sulfur VLSFO.

Beyond the maritime currents, the European natural gas market witnessed a seismic surge of more than 30% on August 8. The tempestuous waves of uncertainty were stirred by apprehensions surrounding diminished LNG supply from Australia, a cornerstone supplier. This unforeseen tempest might have triggered traders to scramble, closing their short positions as they grappled with impending supply constrictions. While Europe’s energy landscape braced for potential winter volatility, the price of LNG as bunker fuel in Rotterdam told a different tale, recording a moderate descent to $648 USD/MT, marking an 18 USD reduction from the prior week. The balance tilted further in favor of LNG, with a price gap of 232 USD against conventional fuel, a testament to the market’s unfolding chapters.

Week 31 introduced a shift in the MDI index’s symphony, where market bunker prices and the digital bunker standard intersect. Ports danced on the fine line between overcharge and underpricing zones. Rotterdam aligned its rhythm with Singapore and Houston, transitioning to the overcharge realm, while Fujairah’s notes of underpricing diminished. VLSFO bore a harmonious underestimation chorus across four ports, with the echoes of change reverberating across Rotterdam, Singapore, Fujairah, and Houston. The MGO LS segment, however, composed a complex melody, with Rotterdam and Houston tuning down the undercharge, while Fujairah orchestrated a different tune, marked by a significant shift.

As maritime enthusiasts scan the horizon for insights, the week ahead beckons with promises of perplexity and promise. The maritime canvas continues to evolve, with the market poised to etch its next distinct trend.

Source: MABUX